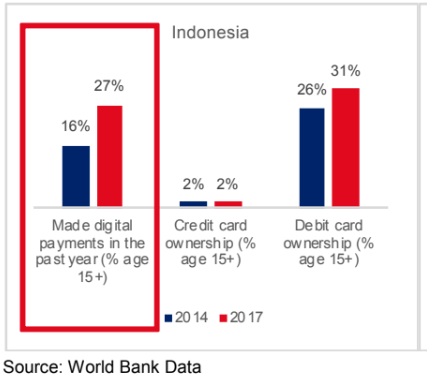

The Indonesian Central Bank repeatedly warns citizens about cryptocurrencies and cautions to understand the risks, but the country’s regulations are currently fairly open towards digital currencies and blockchain technology.

An actual ban only exists for cryptocurrencies in payments, but exchange platforms and ownership of crypto-assets are not. Several state-owned banks and government entities are in fact working on blockchain-based applications, and the country’s financial regulator, OJK, has encouraged this, says Pandu Sastrowardoyo, co-founder of Bali-based blockchain consulting firm Blockchain Zoo.

She points out that to use blockchain technology. Indonesia’s geography – spread across a vast area and many islands – makes it a unique case for implementations of blockchain, explains Sastrowardoyo. Indonesia’s decentralization has led to more regional autonomy, but this came with fragmentation, less oversight, and potential for fraud. It’s quite easy to move to another island with a false identity in Indonesia, Sastrowardoyo says.

Most big banks in Indonesia have announced they’re looking into blockchain technology and are thinking about potential use cases. Blockchain Zoo consults many of them. While she can’t the names involved in individual projects, Sastrowardoyo shared some ongoing blockchain implementations in Indonesia which are likely to launch within the year.

Indonesia’s Blockchain Use Case #1 – Anti Fraud

Image Credit:Freepik

Indonesia has dozens of banks, including regional ones that operate only within a certain province. And not all of them have access to the country’s debt information system, only to bigger ones.

Thus, so-called loan stacking is a concern shared by many smaller banks – when a borrower takes out multiple loans and, in some cases, uses one to pay off another. Without consulting a centralized credit rating system, it becomes difficult to detect these cases.

Blockchain can solve this, Sastrowardoyo explains. A blockchain node is implemented between multiple banks. When people apply for a bank account, their customer information is translated into a unique hash that sits on the blockchain. If the same customer opens accounts elsewhere, the banks can see the hash, and they can flag the customer’s account as a potential for fraud.

Indonesia’s Blockchain Use Case #2 -Branchless Banking

A second application of blockchain that’s already being considered is for ATM machines. “Connectivity in Indonesia has lots of issues,” Sastrowardoyo. “If the connection to one important hub dies, the whole network goes down.”

If you implement a blockchain node on each of the ATMs, even if the main line gets disconnected, the ATMs would still be online and retains some basic functions.

Indonesia’s Blockchain Use Case #3 -Anti Corruption

There are plenty of possibilities for blockchain implementations in anti-corruption management, says Sastrowardoyo. Blockchain can help with increasing transparency, simplifying processes, and getting rid of middlemen. Put into more concrete terms, it often has to do with document management.

“The issue often occurs during the documents exchange,” Sastrowardoyo says. The process takes long, and there’s plenty of opportunity for human error and fraud.

Based on blockchain technology, it’s possible to construct a system that lets companies or different units within an organisation share documents in a secure way, without having the data leave local servers, Sastrowardoyo says. There’s a clear history of all document exchanges which reduces the possibility for fraud.

Indonesia’s Blockchain Use Case #4 -Central Bank Backed Cryptocurrency, Digital Rupiah

Sastrowardoyo confirms that there’s ongoing research looking into the creation of a Digital Rupiah, a cryptocurrency backed by the government. Rumors of this surfaced earlier this year, but the Central Bank later said the plans would not be rolled out anytime soon.

Sastrowardoyo says that what the government is considering is less of a real cryptocurrency, and more akin to an e-money system that runs on the blockchain.

Indonesia could join the short list of countries that already have, or are preparing to issue a state-run digital currency.

Separating the Hype from Real Blockchain Use Cases

These four application scenarios are all useful examples of how Indonesia is thinking about blockchain implementations. As a consultant, Sastrowardoyo has come across instances where companies force the implementation of blockchain, just so they can raise money through and ICO.

Especially when one company owns all the aspects of the process they plan to push onto the blockchain, the technology isn’t necessarily required because it could be solved with simpler tools.

Putting a marketplace that involve different stakeholders onto the blockchain makes much more sense, Sastrowardoyo. That’s what her consulting firm did for FidentiaX, a marketplace for insurance policies based in Singapore. The marketplace digitizes your insurance and you can sell them in bulk. There’s no need for a paper document transfer, which had slowed down the process of previous marketplaces significantly.

“These marketplaces already existed, but with the blockchain, it got much much better,” Sastrowardoyo says. “In my favorite ICOs, the technology is really a differentiator.”

Blockchain Zoo is based in Bali, Indonesia, and was co-founded by a group of entrepreneurs who’ve been part of the blockchain community from early on. The firm was instrumental to the formation of Indonesia’s Blockchain Association last month and works with banks, government entities, and private companies across Southeast Asia.

Featured Image via Freepik

The post How is Indonesia Implementing Blockchain Technology? appeared first on Fintech Singapore.

Avatec provides companies offering financial products with an innovative next-generation credit assessment solution that analyses a broader set of digitized data beyond that which is traditionally used in evaluating personal or business credit applications.

Avatec provides companies offering financial products with an innovative next-generation credit assessment solution that analyses a broader set of digitized data beyond that which is traditionally used in evaluating personal or business credit applications.

Founded in 2017 and based in Jakarta,

Founded in 2017 and based in Jakarta,

Based in greater Jakarta,

Based in greater Jakarta,  The

The